The Turn: Top 10 Work and HR Tech Stories of 2026 (So Far)

It's the end of H1 2026. Let's take stock of what's happened.

I am out of office this week so we have a special edition of The Turn as we look at the top work and HR tech stories of the year so far.

We’re halfway through 2026 and it’s been a helluva half year. So how do you sort through the stories?

Not every big story is actually big. Not every small story is actually small. So I attempted to measure how much a story actually moves the world of work, across six dimensions weighted by how much each one matters.

Reach (25%) — How many workers and organizations are actually touched by this story

Disruption (20%) — How far it breaks from the status quo

Durability (20%) — Whether this is a structural shift or a flash in the pan

Stakes (15%) — The dollar, market, or career magnitude involved

Precedent (10%) — Whether it sets a legal, regulatory, or industry template

Salience (10%) — How loud the industry conversation actually is

Each story is scored 1–10 on each dimension. The weighted scores combine into a single gravity total.

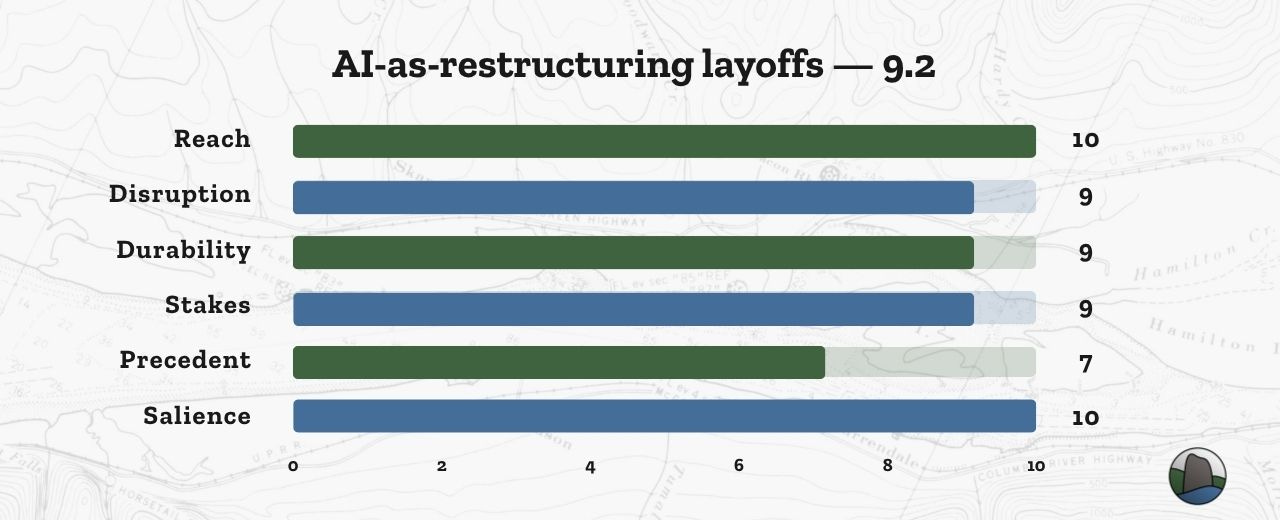

1. AI-as-restructuring layoffs go mainstream

This is the story of the year and it is not close.

Tech layoffs blew past 142,000 in 2026, led by profitable companies cutting to fund a roughly $700 billion AI infrastructure buildout. Amazon eliminated around 16,000 corporate roles. Meta cut around 8,000, about 10% of headcount. Oracle confirmed 10,000 plus. Workday trimmed 1,750 people and called it a reallocation toward AI.

AI is now cited in a majority of layoff announcements, even at companies where the actual automation is still theoretical. Oxford Economics has argued it is often cover for ordinary cost-cutting. Both things are probably true at different companies. What changed in 2026 is that "AI made us do it" became an acceptable public explanation, and companies learned fast that it was a better story than the alternatives.

On reach, this touches the entire labor market at hundreds of thousands of jobs and counting. On disruption, profitable firms cutting to fund AI breaks from the historical norm that layoffs signal distress. On durability, this looks like a structural reset of how companies think about headcount, not a one-quarter event. The stakes are enormous in human terms. And on salience, this is the dominant work-and-AI story of 2026 by a wide margin.

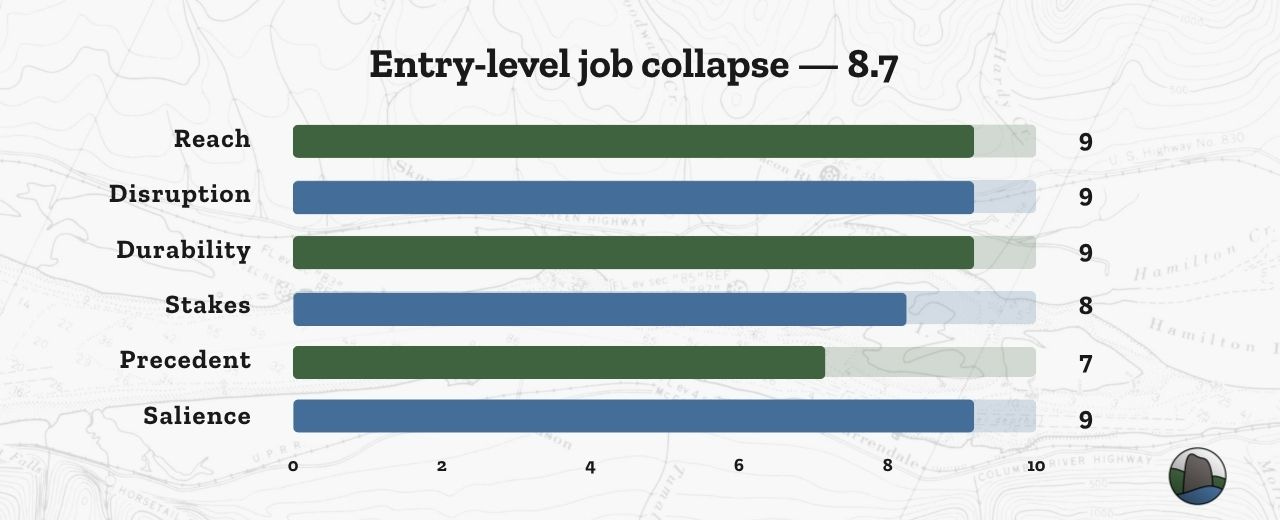

2. The entry-level job collapse

The other half of the AI-and-labor story, and arguably the more consequential one.

New-grad unemployment climbed to roughly 5.6-5.7% against a 4.3% national rate. Underemployment hit 42.5%, the highest since the pandemic. A Stanford Digital Economy Lab paper found a 16% relative employment decline for 22-25 year olds in the most AI-exposed occupations. Entry-level postings are down roughly 35% since early 2023.

The people this is happening to do not have LinkedIn audiences or industry contacts. They just have no way in. The career on-ramp is disappearing, and because it is slower-burning than mass layoffs, it gets less coverage. But the durability score here is high because pipeline damage compounds over years and is slow to reverse. Every year this continues is another year harder to fix.

3. Vendors pivot to a “platform of agents”

The entire HR tech category repositioned this year, from systems of record to what they are now calling systems of agents.

Josh Bersin framed it as the reinvention of Workday, and the product news backs it up. Early adopters are reporting recruiter capacity gains of 54%. Workday has promised 14 new agents by year-end and launched governance tooling including Agent Passport and Agent-Ready Tools to help organizations manage what the agents are actually doing. The Salesforce Agentforce partnership adds another layer to the platform play.

The reach here is significant: eventually this touches every organization running a major HCM suite, and through them most knowledge workers. The disruption score is high because repositioning HR tech from record-keeping to autonomous work execution is a fundamental change to what the category does. And the precedent score reflects that governance tooling like Agent Passport represents an early template for how organizations deploy and oversee AI agents at work. Whether the market is right that digital workers become the next platform layer is still the question. That every major vendor is making some version of this bet is not.

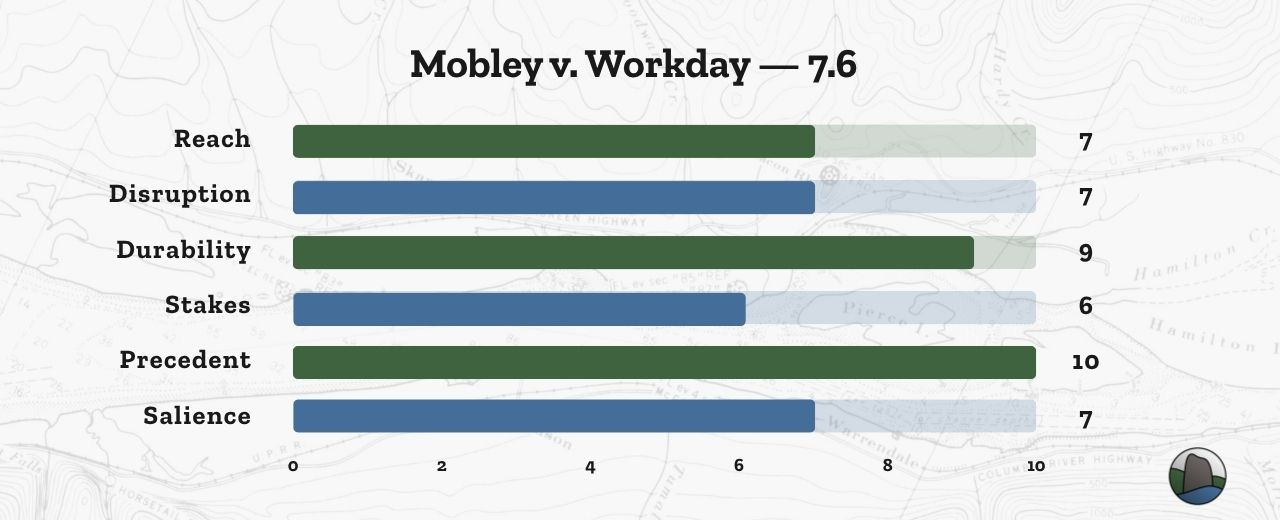

4. Mobley v. Workday sets the AI-hiring precedent

The first real legal template for algorithmic hiring liability.

In a landmark March 6 ruling, a federal court rejected Workday's argument that the ADEA does not cover applicants screened by a third-party system, letting the AI age-discrimination collective action proceed. The opt-in window closed March 7.

What this case is building is the first real legal framework for who is liable when an algorithm filters out a candidate. That answer matters for every vendor selling AI screening tools and every employer running them. The precedent score is the highest of any story on this list for that reason. Case law has long downstream effects, and this case defines the terrain for algorithmic hiring liability in a way nothing before it has. The reach is broad but indirect: any organization using AI in hiring has a stake in the outcome, even if they are not named in the suit.

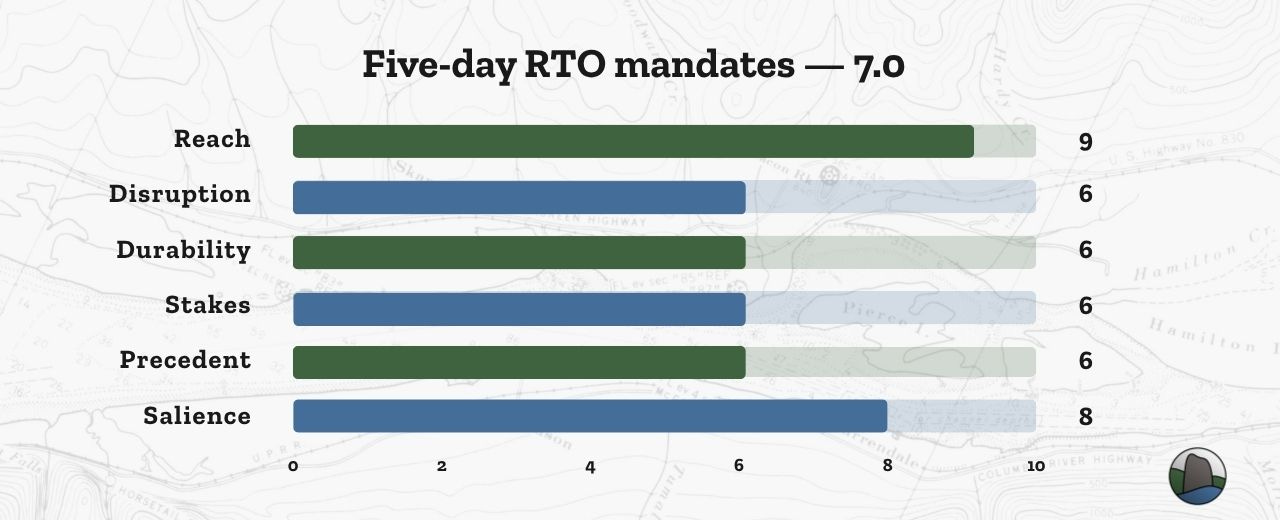

5. Return-to-office hardens to five days

The hybrid detente is over at the top of the market.

55% of Fortune 100 companies now require five-day attendance, up from 5% in 2021. The federal government mandated full return. Roughly 47% of strict-RTO firms say they will discipline non-compliance. Actual measured attendance has barely moved.

The reach here is enormous: this affects huge swaths of office workers and the entire federal workforce. But disruption and durability scores are more moderate, because this is an escalation of an existing fight rather than a new rupture. The hybrid conversation has been going on for four years. What changed in 2026 is that major employers stopped leaving room for negotiation. Whether that holds as the labor market shifts is a different question. For now the mandate went one direction and the behavior went another, and that gap is the whole story.

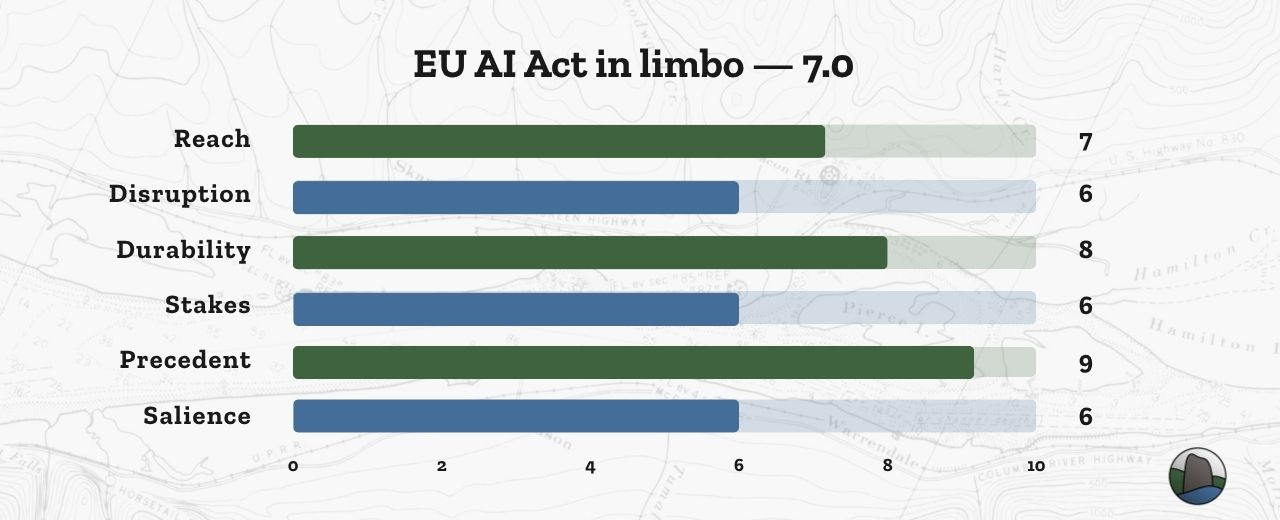

6. The EU AI Act’s employment rules land in limbo

Regulatory whiplash for anyone building or buying hiring AI in Europe.

High-risk employment AI obligations were set to apply August 2, 2026. Then a May 7 provisional Digital Omnibus deal proposed deferring them to December 2027, with the original timeline still in force if the deferral is not formally adopted in time. Fines reach up to 15 million euros or 3% of global turnover.

The uncertainty itself is the story. Compliance teams are now planning against two possible timelines simultaneously. The deferral was supposed to reduce pressure. The result is more complexity, not less. The precedent score here is high because the EU AI Act is the global reference point for regulating employment AI, and what happens with the enforcement timeline will shape how other jurisdictions approach the same question. The framework will govern compliance for years regardless of when the clock starts.

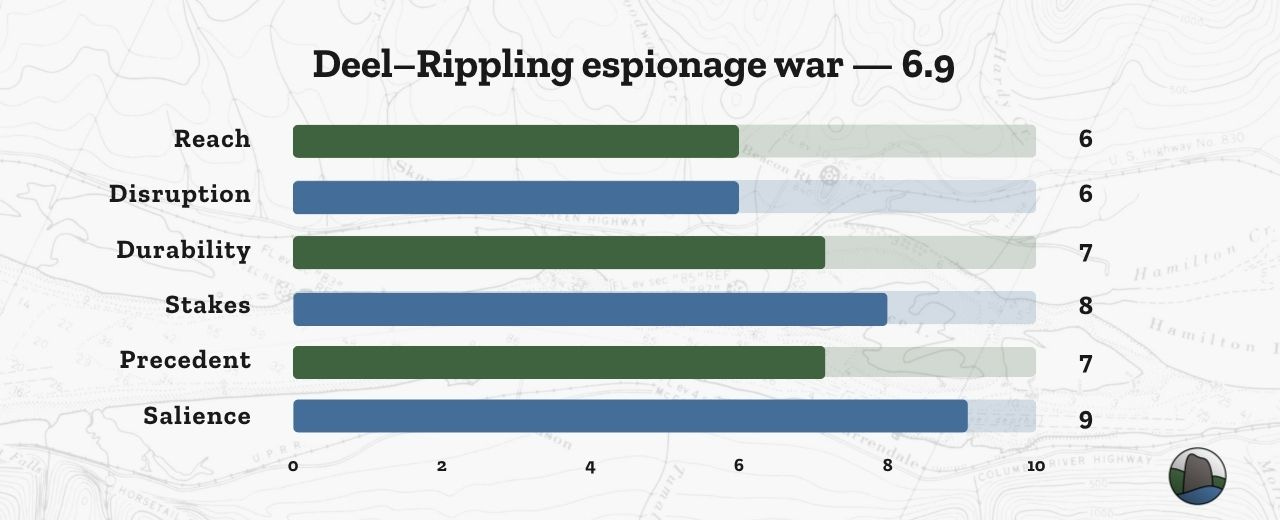

7. The Deel-Rippling espionage war escalates

The juiciest saga in HR tech kept escalating all year.

Federal rulings in February and March let Rippling's RICO and trade-secret claims advance while letting some Deel executives off as individual defendants. Deel filed counterclaims. New banking records surfaced that Rippling says prove Deel paid the person who stole from them. And through all of it, Deel raised $300 million at a $17.3 billion valuation, higher than the year before.

The direct reach is mostly limited to the two companies and their customers. But the stakes are significant: two companies valued around $17 billion each, RICO and trade-secret exposure, and a fundraise that proves the market is not particularly bothered by any of it. The durability score reflects that litigation and reputational effects will run for years. The salience score is the highest of any story in the bottom half of the list. This one has been impossible to ignore.

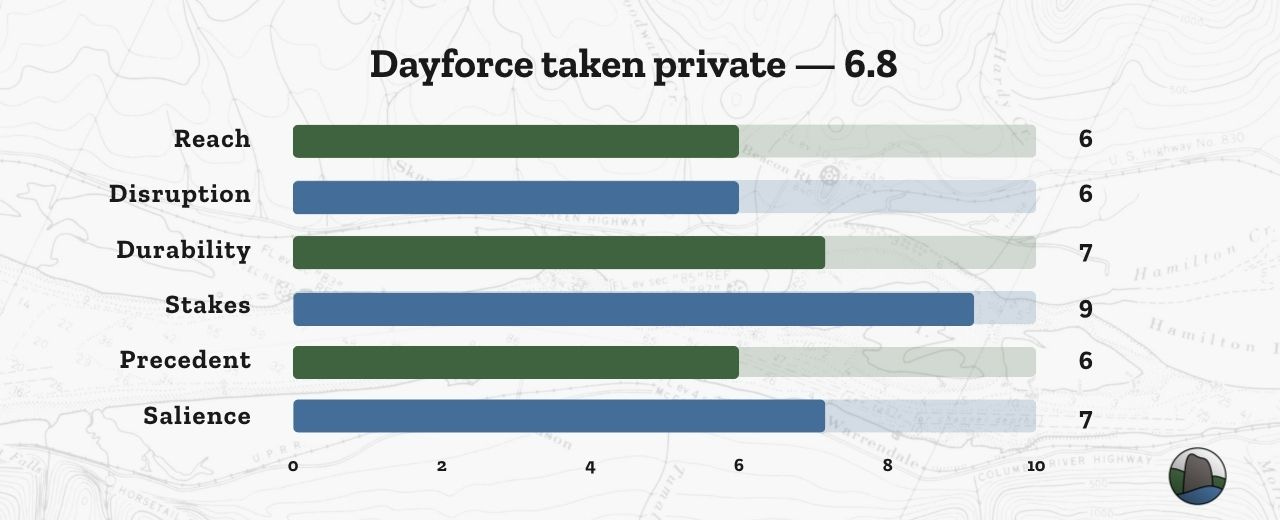

8. Dayforce taken private

The year’s biggest HCM deal.

Thoma Bravo agreed to acquire Dayforce for roughly $12.3 billion including debt, with a minority investment from the Abu Dhabi Investment Authority. The deal is explicitly framed as a bet on expanding Dayforce's AI capabilities in an environment where public market scrutiny makes long-term investment harder to execute.

It ranks eighth. A $12.3 billion acquisition ranks below a lawsuit with no settlement, a mandate nobody is following, a regulatory deadline in limbo, and a corporate espionage saga. That is what happens when you weight worker impact over dollar amount. The stakes score is high, but reach and disruption are moderate: this affects Dayforce customers and the vendor landscape, not workers broadly. PE consolidating HCM is not a new dynamic even at this size. The immediate experience for the average Dayforce user does not change.

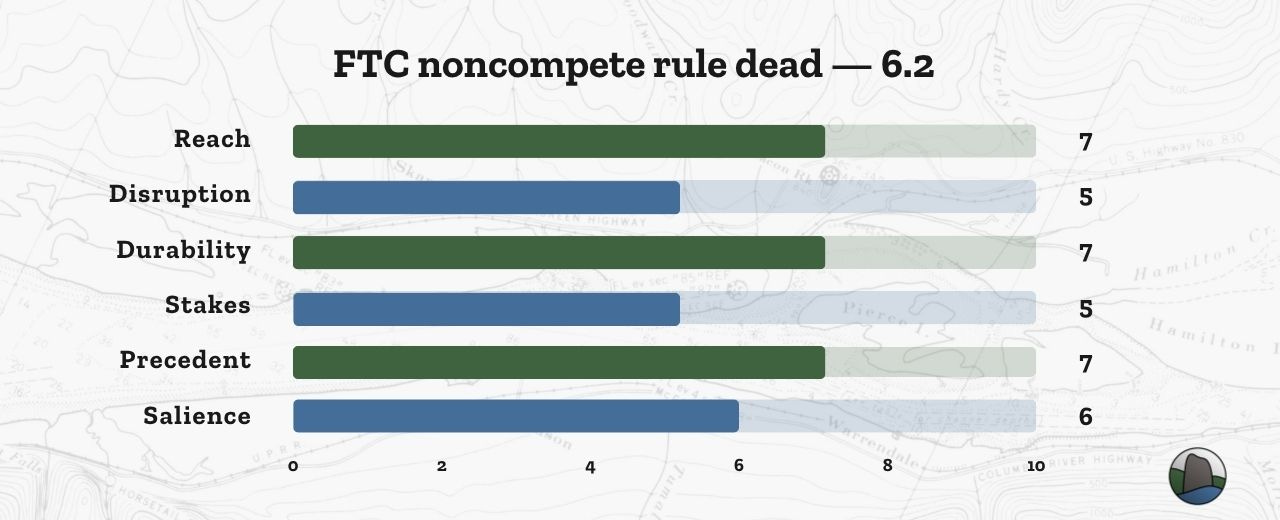

9. The FTC noncompete rule is officially dead

The sweeping federal ban is over.

The FTC formally removed the Non-Compete Rule from federal regulations on February 12 and shifted to case-by-case Section 5 enforcement. A subsequent action against Rollins covered around 18,000 workers, which gives a sense of the scale case-by-case enforcement operates at.

What replaced a national ban is a growing state patchwork that is in some ways messier to navigate than either clean outcome would have been. The workers noncompetes affect most are still subject to them in most states. The reach score reflects that noncompetes touch a large share of the workforce. But disruption scores lower because this restores the prior status quo rather than breaking new ground. The headline moved considerably further than the actual situation did.

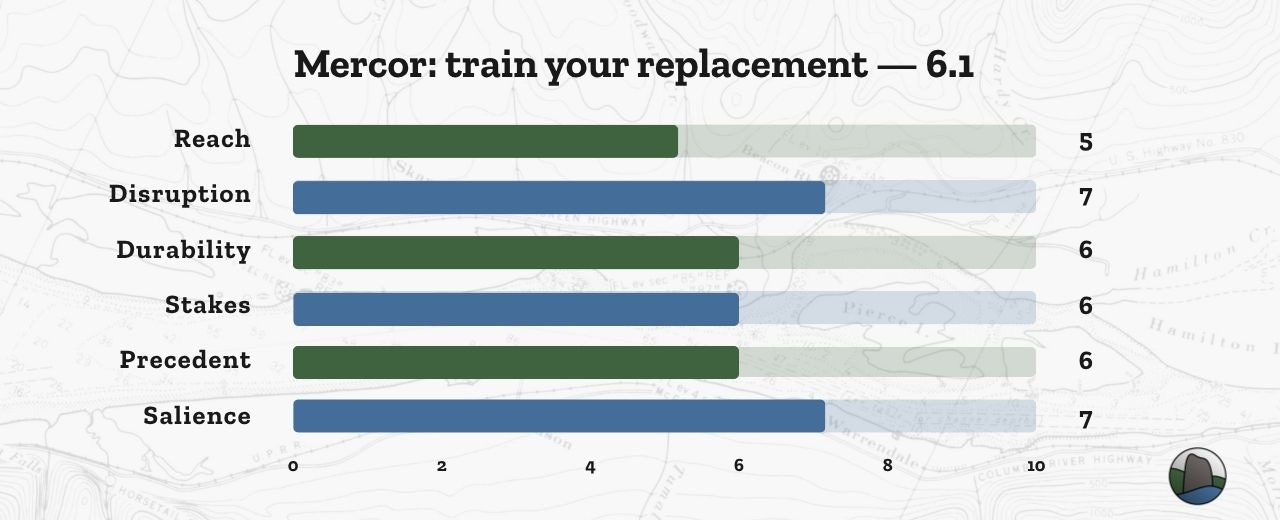

10. Mercor and the “train your replacement” model

A genuinely evolving trend for recruiting and knowledge work.

Mercor, now valued around $10 billion, pays professionals hourly to teach their workflows to AI agents and runs an AI-interview-first hiring process for new roles. The company generated significant attention after Bloomberg coverage in the spring.

The reach score is low today: one company and a niche labor pool. But the disruption and precedent scores reflect what this model represents. Paying people to make themselves replaceable as a product built on top of a hiring platform is a structure that has not existed before. The durability score is moderate because it is still unproven at scale. This earns its spot as a signal of where AI-native work models may be heading, not as a story with current mass impact.

What are your top stories for the year so far? What do you think will happen in the rest of the year?